Farm Financial Analysis Series: Balance Sheet

Financial statements are essential tools for managing farm businesses. Often an accountant or bookkeeper will produce statements from the financial records of the business. Although the manager or owner may not be the person who develops the statements, they should understand the information that the statements provide about the financial condition of the business and be familiar with their options to improve poor financial performance.

This publication is part of the Farm Financial Analysis Series, which also includes P3709 Managing Farm Finances in Turbulent Times, P3710 Cash Flow Statement, P3707 Income Statement, and P3712 Ratios to Measure Farm Financial Health. To ensure you get a full picture of your farm’s financial situation, be sure to use all five publications in the series.

A balance sheet is a snapshot in time of everything owned (assets) and owed (liabilities) by a business. It serves to summarize the financial condition of a business at a point in time and calculates net worth or owner equity by valuing and organizing assets and liabilities. Balance sheets change daily as transactions occur. The “balance” in the balance sheet comes from the requirement that assets = liabilities + owner equity.

In the balance sheet, assets and liabilities are typically broken into current assets and liabilities and noncurrent assets and liabilities. Current assets are assets that are easily converted into cash, so they are either sold or used in 1 year. Current liabilities are liabilities that are paid in the current year. Noncurrent assets are assets that are normally used in the production of the crop or livestock and are not easily converted into cash. This would consist of land and real estate, or it could be capital assets such as machinery, equipment, and breeding livestock. Noncurrent liabilities are liabilities that are due past the current year.

There are two common methods of determining the value of assets: the cost-basis method and the market value method. Cost-basis balance sheets prepared from accounting records show the cost of all assets and the accumulated depreciation of all depreciable assets. The cost-basis value of an asset is commonly referred to as the book value and is useful for tax purposes. Assets may also be valued at market value showing the current value of the assets. The market value method is used in credit analysis when determining the farm’s financial position. Often cost basis and market values are presented in side-by-side columns on the balance sheet.

Balance sheets can be used to measure the financial condition of the business through solvency and liquidity. Solvency measures the degree to which assets are greater than liabilities. In other words, it is the ability to pay off all liabilities if all assets were sold. Liquidity measures the ability of the business to meet short-term financial obligations as they come due without disrupting the normal operation of the business.

Parts of the Balance Sheet

Assets

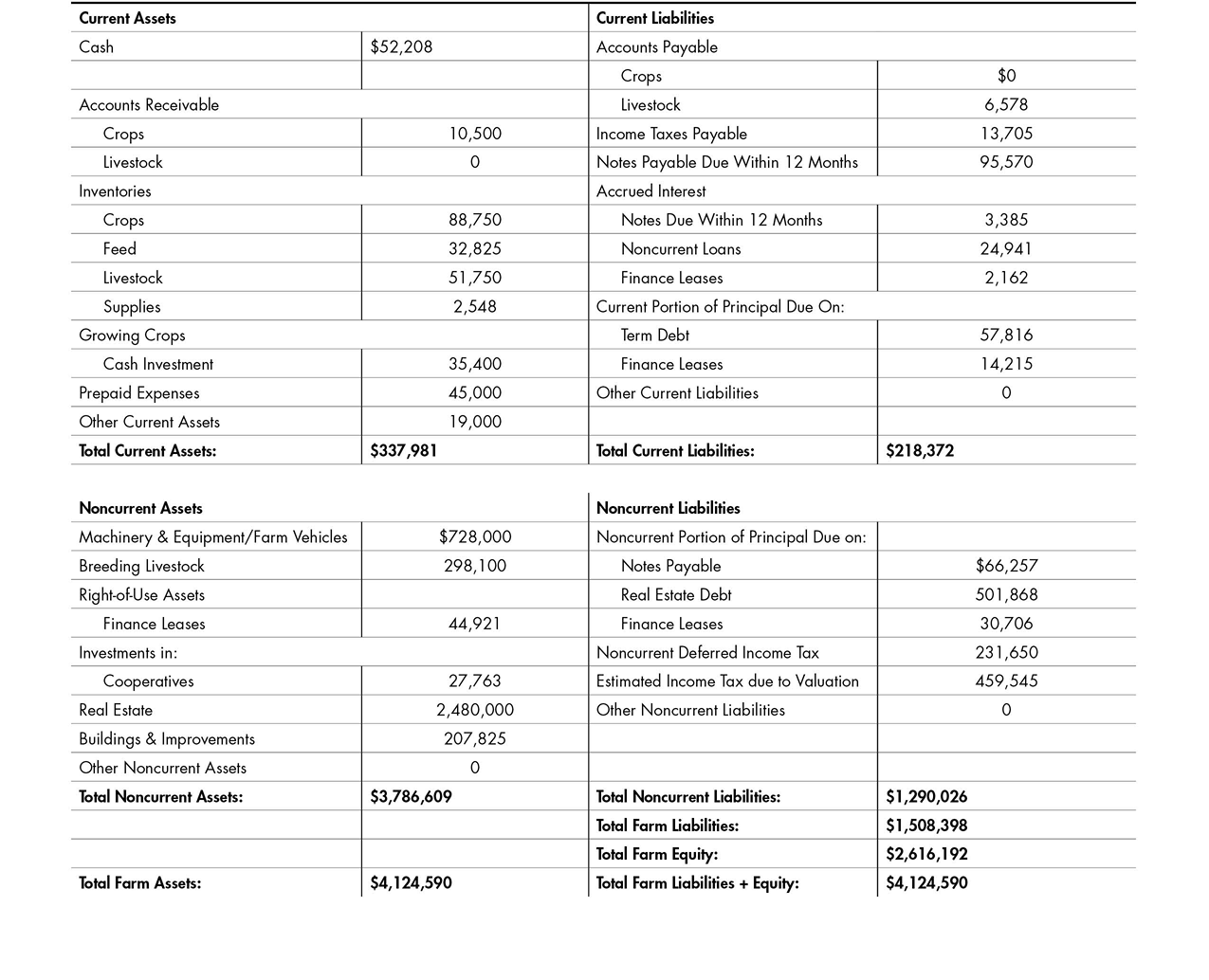

Assets on the balance sheet are items that are owned by the business. Assets are classified given their liquidity as either current or noncurrent assets. Figure 1 is an example of how these assets would be categorized in the balance sheet. Following is an explanation of how these assets are determined given a market-based approach to developing a balance sheet.

Current assets are cash and other assets that are typically used or sold within the year. Current assets include all cash and checking accounts at the time the balance sheet is made. This is typically on the first line of the balance sheet. Accounts receivable includes any items or services that have been provided but not yet paid for. So, if a producer has delivered grain but has not received payment for that grain yet, the transaction is posted to accounts receivable until payment is received, then transferred to cash.

Farm inventories are any stored crops and feed, marketable livestock, and supplies. Stored crops are crops that are easily sold and deliverable. They are valued at the current market price. Feed can either be feed produced by the business, valued at the market price, or purchased feed, valued at the either the purchase price or market value. Marketable livestock is any livestock that is being raised to be sold. It is valued at the market price and an estimate of livestock weight. Supplies are items that are used in farm production in the current year, such as diesel fuel, oil, gas, and tools. The cash investment line under growing crops is any money spent on a currently growing crop. This would be any herbicide, insecticide, fertilizer, seed, or similar cost that has been spent on a planted crop.

A prepaid expense is any money spent on these items for a crop that has not been planted. Fertilizer applied in the fall is considered a prepaid expense until the crop is planted, then it becomes a cash investment.

Other current assets could be items such as a savings accounts, marketable securities, or any other asset that can be quickly converted into cash.

Noncurrent assets are expected to yield services to the business over multiple years. These are assets that are not easily sold (and selling would result in some additional expense). This includes items such as machinery and equipment/vehicles. Breeding livestock are a noncurrent asset as well because they are expected to provide value over a long time period. Breeding livestock include any cows, bred/replacement heifers, and bulls and are valued at the current market price.

A finance lease is a contract for an asset to be used for a specified time period. Real estate is the current market value of any land owned. The current market value of any shops, barns, grain bins, or any other properties that are owned would fall under buildings and improvements. Investments in other enterprises or the value of residence/rental properties would be considered other noncurrent assets.

Liabilities

Liabilities are debts/obligations that are owed by the business. Liabilities are classified by when payments are due as either current or noncurrent liabilities. Figure 1 includes an example of how liabilities would be listed on a balance sheet. Following is an explanation of how various expenses are categorized:

- Current liabilities include accounts payable, or items or goods that have been received but not paid for. In other words, these are items that have been bought on credit.

- Income taxes are also included in current liabilities. These are an estimate of what income taxes will be in the coming year, usually done using the past year’s taxes as a baseline.

- Notes payable is the principal balance of short-term loans, such as an operating loan. These loans typically are for a year or less.

- Accrued interest is the interest due on all farm loans.

- Current portion of principal is the principal payments that will be due within the next 12 months for loans that will be paid off over several years, such as a loan used to purchase land or a lease. Only the portion of the loan due in the next year is included in the current liabilities section.

- Other current liabilities can include things such as ad valorem taxes, deferred taxes, and employee payroll withholdings.

- Noncurrent liabilities are liabilities that will be paid off over several years.

- Noncurrent portion of principal is the total principal payments due after deducting the principal due in the next 12 months.

- Noncurrent deferred taxes include taxable gains on noncurrent assets. Estimated income tax due to valuation is calculated as if assets were liquidated and liabilities paid on the statement date in order to account for income tax requirement under solvency conditions.

Owner Equity

Owner equity is the difference in total farm assets and liabilities. In the example in Figure 1, total farm assets were $4,124,590 and total farm liabilities were $1,508,398. Therefore, owner equity, or total farm equity, was $2,616,192 ($4,124,590 - $1,508,398 = $2,616,192).

How Can a Balance Sheet Help You?

You can use balance sheets to determine if the farm can pay current liabilities without disrupting normal operations caused by selling noncurrent assets and to determine if current and noncurrent debt is properly structured. Comparing farm equity over several years will highlight the progress of your equity in the business. You can prepare balance sheets at any time, but doing so annually at the beginning of the fiscal year provides a consistent measure that can be compared over a period of years to identify trends in the financial health of the business.

Balance Sheet Analysis

Using ratios to analyze balance sheets eliminates the discrepancies between farms of different sizes when using benchmark data. Liquidity is the ability of a business to pay short-term obligations without disrupting the business and is measured with current ratio and working capital.

The current ratio is computed by dividing the current asset value by the current liability value. A value of 1.0 means current liabilities are equal to current assets. Larger ratios are preferred and indicate the ability to provide some safety net if prices change, crops deteriorate, or livestock die. Working capital is computed by subtracting current liabilities from current assets. This shows the amount of cash (current assets) available after paying all current liabilities.

Solvency is the ability of a business to cover all liabilities with all assets and is measured using debt-to-asset ratio, equity-to-asset ratio, debt-to-equity ratio, and others.

Debt-to-asset ratio is computed by dividing total liabilities by total assets and measures what part of total assets is owed to lenders.

Equity-to-asset ratio is computed by dividing total equity by total assets and measures what part of total assets is financed by the owner’s equity capital.

Debt-to-equity ratio is computed by dividing total liabilities by total equity and compares the proportion of financing provided by lenders with that provided by the business owner. Table 1 shows the liquidity and solvency ratios with calculations from the balance sheet in Figure 1.

|

Ratio |

Formula |

Calculations from Balance Sheet |

|---|---|---|

|

Current Ratio |

(Total current farm assets) / (Total current farm liabilities) |

337,981 / 218,372 = 1.55 |

|

Working Capital |

Total current farm assets – Total current farm liabilities |

337,981 – 218,372 = 119,609 |

|

Debt/Asset |

(Total farm liabilities) / (Total farm assets) |

1,508,398 / 4,124,590 = 0.366 |

|

Equity/Asset |

(Total farm equity) / (Total farm assets) |

2,616,192 / 4,124,590 = 0.634 |

|

Debt/Equity |

(Total farm liabilities) / (Total farm equity) |

1,508,398 / 2,616,192 = 0.577 |

Publication 3713 (POD-09-21)

By Brian Mills, PhD, Assistant Professor, Delta Research and Extension Center; Kevin Kim, PhD, Assistant Professor, Agricultural Economics; Kaylee Cooper, Graduate Student (2021); and Jeff Johnson, PhD, Extension/Research Professor (retired), Agricultural Economics.

The Mississippi State University Extension Service is working to ensure all web content is accessible to all users. If you need assistance accessing any of our content, please email the webteam or call 662-325-2262.