Risk Management Options for Family Forests: Timber Insurance

Family forest landowners are generally optimistic people. They manage timber under a number of “acceptable” risks such as fluctuating timber prices, loss from pests, liability, and harvest restrictions. Landowners accept these risks of investment, expecting sizable future timber income that can generate an acceptable rate of return (ROR) relative to the size of their investment.

Ideally, landowners have weighed the costs of economic risks and mitigated against potential loss through improved management and marketing. Many forestry management practices can either minimize or magnify the after-effects of risk factors. For example, the practice of thinning timber can reduce future risk from insects and fire but can temporarily increase the risk from wind and ice damage. Thinning at the proper time and to the right amount is critical.

Extreme weather events represent one of the single-most costly risk factors facing family forest landowners. Unfortunately, landowners in the southern United States live in one of the most risk-prone parts of the country. They face tornados, hurricanes, severe thunderstorms, floods, ice storms, drought, and fire. Between 1980 and 2012, 36 extreme weather events occurred, each causing over a billion dollars in total property damages. Recently, a single 2014 tornado damaged over $14 million in timber.

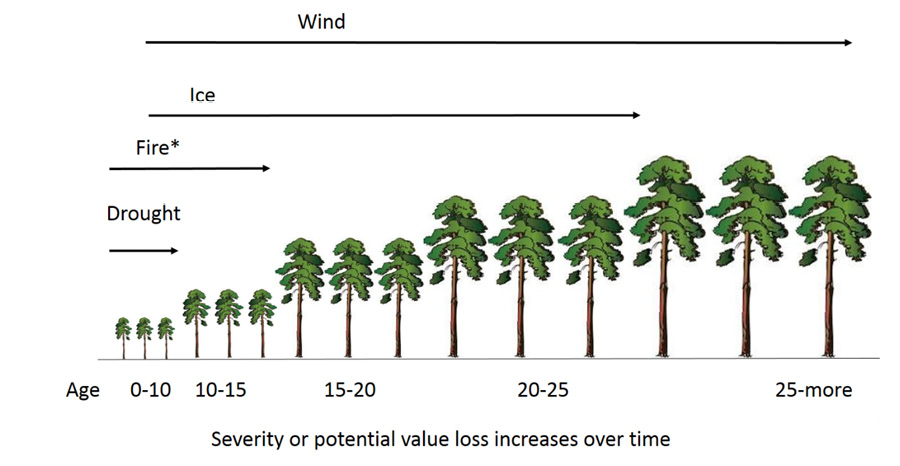

Managing a family forest is a long-term investment, easily exceeding 25 years. Over that period, a forest landowner faces a variety of weather-related risks, and these risks change over the life of a forest (Figure 1). Drought and fire risks are greatest early in the life of a pine plantation and become less risky as the plantation ages, while timber damage risk from wind and ice increases as the plantation ages.

Large-acreage private landowners can reduce their risk by spreading their landholdings over counties and states and by keeping timber stands in different age classes. This diversification of ownership is common among large-acreage private timberland entities such as forest products companies, timberland investment management organizations (TIMOs), and real estate investment trusts (REITs). For them, a single extreme weather event would potentially only damage a small fraction of their holdings. As such, the value loss would be manageable.

Small acreages owned by most family forest landowners will not allow a reduction of risk through diversity. The timber is usually either all young or all old and located in one parcel of ownership. Faced with this situation, landowners may want to consider insurance to address some of their risk of loss. There are two major types of insurance to consider: (1) standing timber insurance and (2) reforestation insurance.

Standing Timber Insurance

Mature pine and hardwood sawtimber that is very valuable and ready for harvest would be an excellent candidate for standing timber insurance. This kind of policy can help protect landowners, who are very dependent on this pending timber income, from a devastating financial loss. Insurance can cover specific perils such as fire, lightning, windstorm, ice, theft, and so forth.

Premiums can increase quickly as you increase the number of perils that are insured against. Cost, therefore, limits most policies to covering only one or two perils. Each peril covered carries an additional premium ranging from 0.5 percent to 1.5 percent of the standing timber value. Premiums can also be greater depending upon how risky your timber is for the peril you are insuring against. For example, protection against wind damage would be more expensive if your timberland were close to the coast.

There are several firms in the southeastern United States that offer this insurance. Standing timber insurance requires a large amount of underwriting information to process an application for coverage. Typical documentation required includes a forest management plan with a detailed timber inventory and property description. Additional information needed may include the number of acres, descriptive information for each stand or tract, type of timber (e.g., pine sawtimber), average age of the timber, distance to the nearest fire department, distance to the coast, and land use information on adjacent property. The application process will also require an estimate of the value of your standing timber and information on any loss in the last several years.

When preparing the application for standing timber insurance, you can estimate the value of standing timber. However, if a damage claim is made, then a certified appraiser must determine the value of the damaged timber. The valuation process considers the market value of the damaged timber at the time of loss and the salvage value of the timber. Additionally, a deductible will be applied, which is typically set at a certain percent of total timber value per risk insured. An example insurance deductible would be 5 percent of total value with a minimum of $500. Deductibles can vary.

Example

A forest landowner owns a 100-acre mature loblolly pine plantation. A final harvest is planned in 3 years, and the landowner wants to insure against a loss until the timber is harvested.

The current pine plantation has 44.7 tons sawtimber, 31.2 tons chip-n-saw, and 20 tons pulpwood and is valued at $1,778 per acre. In this case, a standing timber insurance premium to protect from one peril could range from $8.89 to $26.67 per acre per year, or $889 to $2,667 annually for the 100-acre stand. Annual premiums would be paid for 3 years, until the plantation is harvested. Covered losses during this 3-year period minus salvage income would be reimbursed up to $1,778 per acre minus the deductible.

Standing timber insurance is generally not considered to be a financially viable option over the life of a forest because the premiums paid would negate all potential profits. But, for a short period of time, insurance premiums have little effect on rates of return (ROR) for a timber investment. In the pine plantation example, the estimated ROR was 8.06 percent. Three annual premium payments at the lower 0.5 percent of standing timber value reduces ROR to 8 percent. Premium payments at the higher 1.5 percent of standing timber value reduces ROR to 7.93 percent.

So is standing timber insurance for you? The major factors to be considered in analyzing the feasibility of standing timber insurance are:

- Is there room in your budget for the cost of premiums?

- Is the insurance protection only needed for a short time?

- How critical is the revenue from standing timber toward funding retirement or some other major expense?

- Are you serving in a fiduciary role (e.g., executor to an estate) where the heirs may expect insurance?

Reforestation Insurance

Reforestation insurance is applicable only to pre-merchantable stands and is not intended to insure the value of the trees. Rather, this type of insurance covers the cost of replanting following a catastrophic fire or wind disaster. Reforestation insurance must be renewed annually, but it can provide coverage for as many years as desired.

Reforestation insurance premiums are based on multiple factors, which include past losses, location, total acres, and level of coverage. For example, coverage from one insurance provider is available at either $125 or $250 per acre. Annual premiums for this type of coverage are $1.20 to $1.50 per acre. Deductibles are at 5 percent of the loss (minimum $500) for tracts of less than 2,500 acres. The deductible for larger tracts is 10 percent of the loss (minimum $1,000).

A qualified loss following a fire or wind disaster would have less than 40 percent of the trees survive (e.g., fewer than 200 trees survive from a planting of 500 trees per acre). For the acres so damaged, the insurer would compensate the landowner at the insured amount minus the deductible. Ideally, the insurance payment would cover the cost of reestablishing the lost trees.

Conclusion

Family forest landowners in Mississippi face both economic and production risks that must be factored into forest management decisions. Ideally, the economic risks are deemed acceptable based upon the prospect of future timber income. However, production risks associated with extreme weather events and the worry of timber loss can greatly impair one’s enjoyment of owning and managing timberland. Insurance is an option that family forest owners may want to consider to help address this risk.

Standing timber insurance is an option that can help mitigate potentially ruinous financial loss from damaged timber. A standing timber insurance policy may be practical for those family forest owners whose timber is near financial maturity and the timber harvest revenue is needed for some future expenses (e.g., retirement or college fund). However, standing timber insurance is generally not considered to be a financially viable option over the life of a timber stand.

Reforestation insurance may be a wise choice for those who are very concerned about potential loss of a newly planted or young pine plantation from either wind or fire damage. The right choice will be different for each landowner and each forested property, as each landowner has different levels of risk tolerance, and each property is more or less risky depending upon a variety of factors such as the age and type of timber, species of trees, and location of the property.

The information given here is for educational purposes only. References to commercial products, trade names, or suppliers are made with the understanding that no endorsement is implied and that no discrimination against other products or suppliers is intended.

Publication 2911 (POD-09-21)

Reviewed by Shaun Tanger, PhD, former Assistant Professor, Coastal Research and Extension Center. Written by James E. Henderson, PhD, Professor and Head, Coastal Research and Extension Center, and Linda W. Garnett, former Extension Associate, Forestry.

The Mississippi State University Extension Service is working to ensure all web content is accessible to all users. If you need assistance accessing any of our content, please email the webteam or call 662-325-2262.