Economic Impact of the Southern Producers Replacement Heifer Sale

In today’s world of increasingly limited public funding, more attention is placed on the value that public programs have on specific audiences and society. Policy makers, public leaders, and the public rightfully demand assurance that public investment into these programs and activities is actually beneficial.

This scrutiny rightfully includes Cooperative Extension. Extension draws its base resources from three distinct levels of public funding: federal, state, and local. In the case of many of its programs, Extension programs are examined by all three governmental levels to ensure that a positive return on public investment is being realized.

One of the more effective tools that can be used to evaluate the efficacy of Extension programs is economic impact analysis. While a detailed description of this methodology is beyond the scope of this publication, economic impact analysis examines an economic event or “shock” to a local economy and estimates the economic spillover benefits or costs that occur in the areas of spending, employment, employee wages, proprietor income, and the additional value that is added to the economy. A demonstration of this type of analysis to the evaluation of an Extension program is applied to the Southern Producers Replacement Heifer Sale.

History of the Sale

In 2001, Mississippi State University Extension Service agents organized and conducted the first Southern Producers Replacement Heifer Sale (SPRHS) as a means for beef cattle producers in south Mississippi to market top-quality replacement bred heifers. Many heifers marketed through this auction have been homegrown by cattle producers and each heifer must meet a rigid set of quality and assurance standards, including confirmation of pregnancy within 30 days of the sale date through palpation by a certified veterinarian. Heifers are also pelvic measured and screened for obvious defects and other problems that might exist. These standards have been developed by Extension personnel through strong collaboration with producers and, through the efforts of Extension personnel to maintain rigorous quality standards and marketing of the sale, buyers have been willing to pay a premium over average commercial bred heifer prices.

These premiums attract both buyers and sellers of high-quality breeding heifers. Consignors are established producers and the majority have been involved in this sale for several years, thus sustaining a reputation for producing superior quality breeding stock. Though this sale is a way for producers to earn a premium on their finest heifers and increase revenues, a critical question remains concerning the economic impact that these economic benefits have on the rest of the state’s economy. Using the IMPLAN software to implement input-output analysis (economic analysis), we estimated the indirect and induced effects of the sale’s economic impact to estimate the economic benefit that is derived from the premium attached to the sale of these cattle.

Scope of the Analysis

The analysis has three goals. First, we estimate the marginal (additional) revenue obtained from marketing animals through the SPRHS as compared to replacement female breeding stock marketed through more common commercial auctions held throughout the state. Second, we use economic impact analysis to estimate economic spillover benefits that result from the change in revenue due to the producer participating in the sale. Finally, an overview of the procedure used to evaluate the economic impact of an Extension program is presented.

Data

Prices for individual animals marketed through the sale were obtained for each SPRHS auction from 2016 through 2021. The information was categorized by consignor and included each individual animal’s total sale price. Other details such as breed, weight, stage of pregnancy, and age were not included in the transaction data.

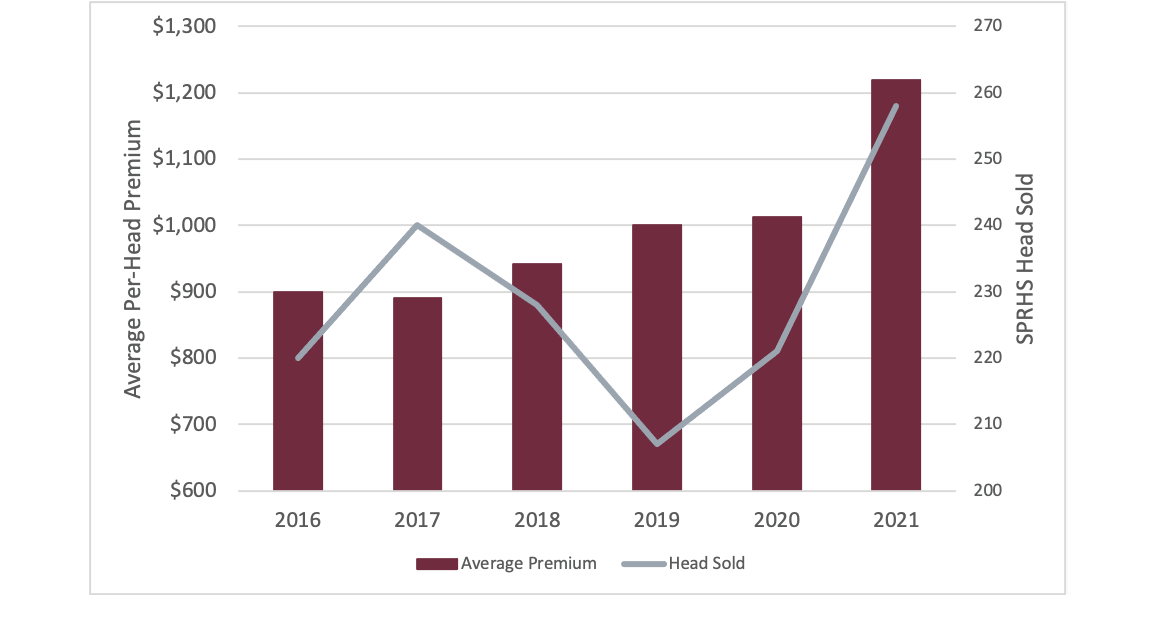

Figure 1 shows the number of head sold through the SPRHS sale and the average premium per head earned by participating in the sale. While the number of head entering the sale hit a low for the six-year study period of 207 head in 2019, a six-year study period high number of head marketed (258) was achieved in 2021. In addition, the average per-head premium for those producers participating in the sale increased from a low of $890 in 2017 to a high of $1,219 in 2021. This suggests that the reduction in supply for the national bred heifer market has, to some degree, resulted in higher prices for quality replacement stock.

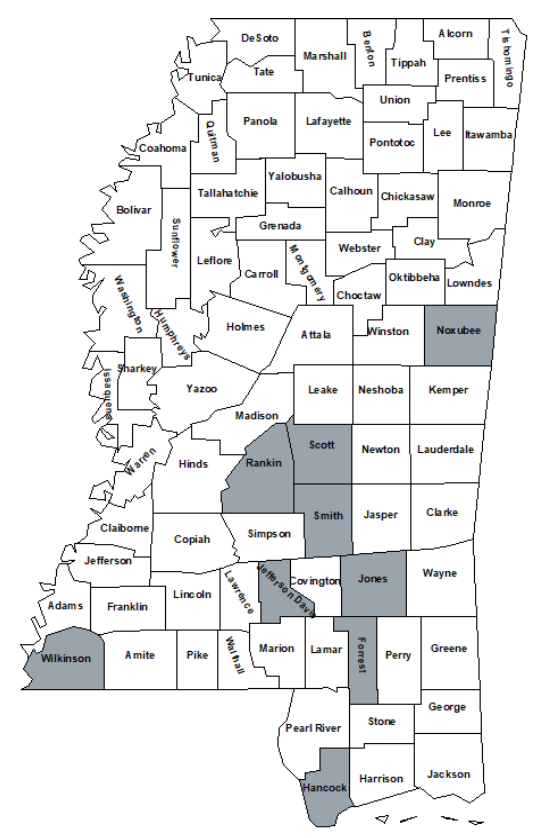

Figure 2 presents the counties in which cattle operations that participated in the SPRHS sale from 2016 to 2021 are located. Most cattle operations that participated in the SPRHS are based in the south-central portion of the state, but cattle producers from other counties make a relatively large investment in transportation to deliver animals to the sale. It is important to note that several counties had more than one producer participate in the sale.

Baseline commercial market data was gathered from two separate time frames during which the format of reported data changed significantly. Data from 2016 through 2019 consisted of weekly statewide statistics published by the Mississippi Department of Agriculture and Commerce (MDAC) and the USDA Agricultural Marketing Service (AMS) for female breeding stock. These data contained the weekly low, weekly high, and average prices for small/medium frame and medium/large frame cow-calf pairs. These pairs would not include heifers and replacement animals which would include heifers, but also cows which would have had a calf at some point. Since these data did not contain information regarding age, weight, breed, pregnancy status, or the number of head that were sold each week, the averages of all weekly sales for the entire state for each year of the timeframe were averaged to determine a baseline price for each year.

In 2020, AMS changed the data collection and reporting system. This change resulted in a much richer data set in which bred heifers and cows were classified as distinct categories and sale data was reported by location, number of head in each lot, frame size, muscle grade, age, pregnancy status, minimum, maximum, and average weights of the lot, and the minimum, maximum, and average sale price per head for each lot. Bred animal sales were reported for 13 sale locations1 across the state in 2020 and 2021.

However, there seems to be discrepancies in the reported data regarding whether specific animals were heifers or cows. To alleviate this potential problem, a weighted average of the per head selling price for all bred stock under two years of age was calculated and used as the baseline comparison for 2021.

Descriptive statistics for the SPRHS sale and commercial market sales baseline data for each year are provided in Table 1. The estimated average premium for participating in the SPRHS was calculated by subtracting the Mean Commercial Sale Baseline Price/Animal from the Mean SPRHS Price/Animal and ranged from $900 in 2016 to $1,219 in 2021 with the average premium per SPRHS animal sold increasing each year after 2017. Note that the SPRHS premiums are aggregate in nature and do not necessarily identify the true magnitude of the price difference if the same SPRHS cattle would have been sold at a commercial auction. Unfortunately, the data do not allow for a more extensive analysis. Suffice it to say that the heifers committed by the cattle producers to the SPRHS are of higher-than-average commercial quality and garner an above-average commercial price.

|

Statistic |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

All Years |

|---|---|---|---|---|---|---|---|

|

Number of SPRHS Head Marketed |

220 |

240 |

228 |

207 |

221 |

258 |

1,374 |

|

Median SPRHS Price/Animal |

$2,050 |

$1,800 |

$1,800 |

$1,800 |

$1,900 |

$1,900 |

$1,900 |

|

Mean SPRHS Price/Animal |

$2,043 |

$1,824 |

$1,858 |

$1,857 |

$1,946 |

$2,009 |

$1,922 |

|

Mean Commercial Sale Baseline Price/Animal |

$1,143 |

$934 |

$912 |

$856 |

$933 |

$790 |

$9282 |

|

SPHRS Sale Price Standard Deviation |

$243 |

$237 |

$183 |

$207 |

$229 |

$419 |

$282 |

|

Average SPRHS Premium/Animal |

$900 |

$890 |

$942 |

$1,001 |

$1,013 |

$1,219 |

$998 |

|

Total SPRHS Premiums |

$197,990 |

$213,540 |

$214,852 |

$207,108 |

$223,807 |

$314,380 |

$1,371,677 |

1 Sales locations reporting bred animal prices for 2020 and 2021 included the Brookhaven Stockyard; Cattlemens Livestock (West Point, MS); Grenada Stockyard; Lipscomb Brothers (Jackson, MS); Lucedale Stockyard; Macon Stockyard; Meridian Stockyard; Peoples Livestock Auction (Houston, MS); Philadelphia Stockyard; Southeast Livestock Exchange (Hattiesburg, MS); Tadlock Stockyards (Jackson, MS); Tylertown Stockyard; and Winona Stockyard.

2 The mean commercial sale baseline price per animal is calculated as the average of the average price for each of the years in the study period.

The estimated standard deviations for the baseline commercial cattle were fairly consistent across the years with the exceptions of 2018 and 2021; 2018 exhibited a tighter grouping of per head prices than did the other years while prices in 2021 had substantially more variation than did prices in other years. The Total SPRHS Premium represents the estimated total level of premiums paid to cattle producers who participate in the SPRHS sale and measures the direct effect or the increased level of income realized by the producers for each year. The Total SPRHS Premiums reveal that an estimated $1,371,677 in premiums were paid to producers over the six-year study time frame.

Analysis

While the direct effect of the SPRHS was estimated to have increased participating cattle producers’ incomes by $1,371,677 over the six-year study period, there are other economic effects and variables that should be examined to completely evaluate the program. Economic impact analysis is a methodology well suited to estimating these effects and the IMPLAN® software is a well-recognized proprietary software package that is designed to perform this type of analysis (Johnson, 1986).

A common metric used by economic development professionals and community leaders is “economic spillover.” Economic spillover of an economic shock is determined by summing the estimates of the indirect and induced effects.

Indirect effects represent business-to-business transactions made by the sector being examined. For example, an operation may purchase feed from the local agricultural cooperative, medicine from a local animal health supply store, fuel from a local fuel station or distributor, and building supplies from the local hardware store. Induced effects represent the household-based purchases made by the employees and owners of the businesses involved in the direct and indirect transactions. Examples include groceries, clothing, medical services, and automobile purchases for personal use. The sum of the indirect and induced effects is commonly referred to as economic spillover.

IMPLAN also estimates several economic variables within the direct, indirect, and induced effects. These include the following:

- Employment – the number of full- and part-time jobs that result from the initial shock (direct effect) in the local economy.

- Labor income – the level of wages and salaries (including proprietor income) paid to employees and proprietors.

- Value added – the amount of value that is added to raw inputs in the part of the production process that takes place in the local economy.

- Output – equivalent to sales.

Given the type of economic information under consideration, a critical decision must be made regarding the method used in analyzing the economic shock/stimulus (the premiums to cattle producers earned from heifers being marketed through the SPRHS). In the input-output methodological framework, these premiums can be treated either as a change in the beef cattle production industry or as a change in household income.

The major difference between these approaches concerns an implied change in the production practices utilized by cattle producers. Modeling the premiums as an industry change would generate indirect (business-to-business) effects in additional to induced (household-level purchases made by employees and business owners). An underlying assumption that could easily be made is that an individual cattle producer is changing production practices as a result of the increased income received from the premiums. While this scenario is certainly a possibility, it should be recognized that a change in production practices would likely lead to increased production by the producers participating in the SPRHS, but there is no indication of this from the available data.

Modeling the economic effects of the increased premiums as changes in household income eliminates any indirect effects from consideration. This option generates only household-level purchases and thereby implicitly assumes that there is no change in production practices. In addition, given the available data, this estimation method results in more conservative and defendable estimates.

The question then arises as to which operations choose to reinvest some of the SPRHS premiums in the business and which opt to spend all the premiums on household expenditures (for example, take a vacation or purchase a new living room suite). After examining the distribution of the number of head sold per operation each year, we decided to use 10 head sold each year through the SPRHS as a threshold. If an operation sold fewer than 10 heifers each year, then we assume that the change in revenue (premium) from the sale is small enough that the proprietor will use the entire amount for household expenditures. If the operation sold 10 or more head within a given year, we assume that a portion of the premiums will be reinvested in the business.

This decision to segregate the operations by the number of head sold spawns several analysis decisions. Since we are assuming that there will not be a noticeable increase in cattle production due to the SPRHS premiums, we model the increase in proprietor income for operations selling 10 or more head each year as an industry change for IMPLAN Sector 11 – Beef cattle ranching and farming, including feedlots and dual-purpose ranching and farming. We specified industry sales as the aggregate level of premiums received by this class of operations for the specific analysis year. Since we assume that there will be no appreciable increase in production, and that we are estimating marginal (additional) changes in economic activity, the level of employment was constrained to zero employees and the level of employee compensation was constrained to $0. The level of proprietor income was assumed to be the same as the level of sales since the change in sales necessarily equals the change in proprietor income.

The modeling of the change in proprietor income for those operations that were assumed to not reinvest the SPRHS premiums into the firm (operations selling fewer than 10 heifers through the SPRHS in a given year) is more complicated. Since the USDA Economic Research Service estimates that the median level of farm household income ranged from $76,250 in 2016 to $83,111 in 2019 (the latest year for which these estimates are available), we modeled this change in household income in the $70,000-$100,000 household income range provided by the IMPLAN software.

We then estimated the amount of federal and state and local taxes that needed to be deducted from the gross premium to determine the level of disposable spending that could take place. To estimate the federal taxes, we calculated the proportion of Federal Government Nondefense spending (this spending is presumed to be derived from federal tax collections) as a part of total household spending for the $70,000-$100,000 household income range using estimates provided by the IMPLAN software.

The level of estimated federal taxes was deducted from the total level of premiums earned by the operations with SPRHS sales under 10 head for each analysis year. The same type of methodology was used to estimate the level of state and local taxes, except that the level of State/Local Government Non-Education expenditures was used as a proxy for the total level of state and local taxes paid by households in the $70,000-$100,000 income range. The estimated level of state and local taxes and federal taxes were deducted from the level of premiums received for this class of operation for estimation of the induced effects.

The estimated aggregated direct state, local, and federal taxes were apportioned among the appropriate fiscal revenue source categories by using the induced effects tax tables from operations selling 10 or more head analyses for each year of the study period. This set of estimations was used as a guide due to the relatively large level of direct effects and the assurance that these large levels would populate the induced effects tax tables (recall that the induced effects represent household purchases by employees, the same concept being considered when the entire amount of SPRHS premiums is being used for household purchases).

Economic impact analysis summary results are shown in Table 2. While the increases in the number of jobs created attributable to SPRHS premiums are relatively small for all years, labor income net of changes in proprietor income (calculated by subtracting “Direct proprietor income change net of taxes” from “Change in labor income”) experienced increases from $30,959 (2019) to $87,853 (2021) as a result in the increases in farm household income. In addition, the state’s value-added activities net of the direct increase in proprietor income from a low of $94,567 (2019) to a high of $199,013 (2021). We estimate that the total level of sales increased for all sectors increased by $2,955,591 over the study period, including the changes in proprietor income net of taxes and that the level of sales due to the economic spillover effects increased by $1,589,804.

|

Changes |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

Total |

|---|---|---|---|---|---|---|---|

|

Direct proprietor income change net of taxes |

$195,512 |

$213,373 |

$213,964 |

$206,216 |

$222,946 |

$313,776 |

$1,365,787 |

|

Change in employment |

2.7 |

2.6 |

2.4 |

1.7 |

2.1 |

3.0 |

14.5 |

|

Change in labor income |

$253,227 |

$282,166 |

$260,670 |

$237,175 |

$268,297 |

$401,629 |

$1,703,164 |

|

Change in value added |

$345,038 |

$398,672 |

$348,202 |

$300,783 |

$345,160 |

$512,789 |

$2,250,644 |

|

Change in output |

$460,775 |

$491,181 |

$486,463 |

$390,467 |

$455,680 |

$671,025 |

$2,955,591 |

The use of the IMPLAN software also allows the estimation of fiscal (tax) effects that accrue to local, state, and federal governments each year for the induced effects. These effects are shown in Tables 3 and 4. While the induced household income change effects and industry change effects are gathered directly from IMPLAN, additional steps are taken to gather the direct effects of the household income change. The first step is to calculate the proportions of household income changes paid directly to state, local, and federal taxes. This is done by dividing the amounts paid for federal (non-defense) and state (non-education) by the total state, local, and federal taxes for a given year. Once these proportions are found, the remainder of household income is run through IMPLAN to receive the induced tax effects.

While most of the changes in taxes in Table 3 are paid to the Mississippi Department of Revenue and are used for state-level programs that benefit the residents of the state, there are two sources of revenue that accrue to local governments. Property taxes, whether personal property taxes or property taxes derived from taxes on production and imports (TOPI), generally accrue to local (county and municipal) governments. The total increase in taxes accruing to state and local governments is $118,383 (Table 3) and the total increase in taxes accruing to the federal government is $220,934 (Table 4).

|

Category |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

Total |

|---|---|---|---|---|---|---|---|

|

Social insurance |

$6 |

$6 |

$6 |

$3 |

$5 |

$7 |

$33 |

|

TOPI: Sales tax |

$8,718 |

$10,566 |

$11,516 |

$2,856 |

$4,000 |

$5,377 |

$43,033 |

|

TOPI: Property tax |

$5,133 |

$6,286 |

$6,883 |

$1,704 |

$2,387 |

$3,208 |

$25,061 |

|

TOPI: Other taxes |

$1,103 |

$1,066 |

$1,159 |

$287 |

$400 |

$539 |

$4,554 |

|

Personal Tax: Property tax |

$100 |

$128 |

$125 |

$243 |

$274 |

$411 |

$1,281 |

|

Personal Tax: Other taxes |

$5,475 |

$6,456 |

$5,767 |

$5,287 |

$5,971 |

$8,946 |

$37,902 |

|

Corporate profiles and dividends |

$1,081 |

$1,152 |

$811 |

$885 |

$1,054 |

$1,536 |

$6,519 |

|

Total |

$21,616 |

$25,660 |

$25,456 |

$11,265 |

$14,091 |

$20,024 |

$118,383 |

|

Category |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

Total |

|---|---|---|---|---|---|---|---|

|

Social insurance |

$16,172 |

$16,576 |

$15,636 |

$13,274 |

$15,445 |

$22,779 |

$99,882 |

|

Taxes on Production and Imports |

$1,892 |

$2,037 |

$2,539 |

$684 |

$958 |

$1,288 |

$9,398 |

|

Corporate Profits Tax |

$4,949 |

$4,368 |

$1,445 |

$1,826 |

$2,172 |

$3,167 |

$17,927 |

|

Personal Income Tax |

$13,189 |

$16,410 |

$14,705 |

$12,933 |

$14,606 |

$21,884 |

$93,727 |

|

Total |

$36,202 |

$39,391 |

$34,325 |

$28,717 |

$33,181 |

$49,118 |

$220,934 |

Furthermore, while sales taxes collected by businesses are remitted to the Mississippi Department of Revenue, 18.5 percent of sales tax collected within an incorporated municipality’s boundaries (city/town limits) are remitted back to that municipality’s general fund as a diversion. There is no diversion to counties for sales tax collected from outside municipal boundaries.

Additional federal taxes collected that are attributable to the SPRHS premiums also tended to increase in two cycles over the study period. The decline in tax collections that occurred in 2019 was likely due to federal tax cuts imposed at the federal level. It should be noted that once these tax cuts were implemented, tax collections resulting from the sale premiums rose.

Conclusions

The primary goal that spurred the development of the Southern Producers Replacement Heifer Sale was to provide an opportunity for producers of high-quality breeding stock to generate revenues above what could be earned by placing these animals in regular commercial auctions. Our estimates show that this goal has been met with an average $1,299 premium per head sold over the entire study period, but there are other considerations that make this Extension-related program even more valuable to the state of Mississippi as a whole.

This analysis reveals that substantial economic spillover benefits exist, resulting from the estimated induced effects, associated with increasing producer household incomes due to participation in the SPRHS. Indirect and induced employment effects revealed an estimated increase of 14.5 full- and part-time jobs, the estimated indirect and induced labor income effects revealed an increase in labor income of $475,250 and the estimated indirect and induced effects for value-added activities in the state revealed an increase of $858,052. In addition, indirect and induced sales effects in the state were estimated to be $1,746,806 due to the SPRHS premium increases.

Economic evaluation of Extension programs

While one purpose of this study was to estimate the direct and economic spillover benefits of a recognized Extension programming activity, another purpose is to advise the reader regarding critical factors to be considered in developing an economic impact evaluation of Extension programming. We encourage anyone who is considering this type of analysis to consider the following factors:

- Determine if the Extension program can be appropriately evaluated using the economic impact analysis methodology. This methodology involves spending by some party. The analysis presented in this publication involved spending by purchasers of replacement breeding stock both at the SPRHS sale and through commercial sales. This type of analysis may not be appropriate or may not be feasible for some types of Extension programs, such as an evaluation of the leadership skills gained by 4-H club members due to the types of research and assumptions that would be involved in a rigorous analysis.

- This type of methodology cannot determine the feasibility of a project. Economic impact analysis cannot indicate whether a project or program is profitable or even if the economic benefit of the program exceeds its economic costs. Economic impact analysis can be used to estimate the indirect and induced (economic spillover) effects of the program’s profits and losses or excess economic benefits/costs if the condition regarding spending discussed above is met.

- Analyze the economic impact of the project correctly. It is very easy to misuse this type of analysis methodology and obtain inaccurate numbers that can mislead policymakers. Having the analysis reviewed by competent practitioners of the methodology will not only ensure that the analysis is as accurate as possible, but will also provide a high level of transparency to potential users. There are several Extension and research economists associated with the Mississippi State University Department of Agricultural Economics or Department of Forestry that can assist in providing objective analyses of this type.

- Beware of the temptation to generate large economic multipliers. While a technical discussion of the concept of economic multipliers is beyond the scope of this analysis, they are basically ratios that measure the magnitude of the total economic effect for the various economic variables as compared to the direct effect. While the IMPLAN software can generate large multipliers, these cannot objectively be defended. In general, a multiplier or ratio of 2.0 is considered to be close to the highest defendable level and production agriculture multipliers are generally well below that level. The labor income multiplier for the operations that sold 10 or more heifers through the SPRHS is calculated as 1.36 (realizing that proprietor income is a part of labor income).

However, the assumptions made in developing the analysis will result in multiplier increases or decreases. While the labor income multiplier is calculated to be relatively low, the output or sales multiplier for operations that sold 10 or more heifers in the sale for 2020 is estimated as 2.23. This relatively high estimation is due to the assumption that the change in proprietor income would not change the operations’ production practices, so no additional labor would be hired and thus there would be no additional employee wages (costs that would reduce the operations profits and proprietor income) resulting from the increase in revenue. - Utilize reputable data sources. The analysis presented in this publication utilized objective data provided by the Southeast Mississippi Livestock auction barn (home to the SPRHS) and the USDA Agricultural Marketing Service. While the deficiencies of the AMS data were previously discussed, these organizations provide objective records of expenditures that add to the objectivity of the analysis. While collecting these types of data can be tedious and time-consuming, utilizing these types of data provides a more objective basis for analysis than producer surveys or anecdotal evidence.

- Report the results of the analysis objectively. It is likely that any type of analysis or evaluation of this type will be read with interest by several stakeholders in the local community. It is important that the evaluation results be reported as objectively as possible.

The example used in this publication provided a number of points that could be used to demonstrate the economic impact of this Extension program. First, animals sold through the SPRHS received a high premium; this obviously benefits the producer that sold the animal. In 2021, 15 individual producers sold between four and 47 head of replacement heifers. This suggests that these producers earned between $4,876 and $57,293 in premiums over the average replacement heifer sold at a typical commercial sale. It is possible that these animals could have commanded a premium at a commercial sale; however, the available commercial sale data does not identify premium cattle.

The story does not end here. We estimate that the estimated premiums generated by the sale of 258 quality replacement heifers in the 2021 SPRHS generated an additional $1,746,806 in sales (output) from business-to-business and employee spending, as well as an additional 14.8 jobs earning $475,250 in labor income throughout the state. It is assumed that the average additional job earned 32,111 in wages/salaries and benefits.

There are also substantial fiscal effects that further demonstrate the value and impact of the Extension program to elected officials. We estimate that the premiums earned from participation in the 2021 SPRHS generated an estimated additional $20,024 in total state and local taxes. While the state government receives the bulk of these revenues, local governments typically receive property taxes ($3,619) and municipalities receive an 18.5 percent diversion of the sales tax that is collected within municipal boundaries that supplements their general fund.

Given that municipalities collected 84.5 percent of the sales tax collected in the state for the most recent 12 months, we estimate that premiums received from the 2021 SPRHS resulted in an increased diversion to municipalities of $841. This suggests that local governments received an additional $4,460 and the state government received $15,564 to enable programs that benefit the public good (such as Cooperative Extension). In addition, SPRHS premiums generated an estimated additional $49,118 in federal revenues.

We conclude with the presumption that most Extension programs have economic benefits that could be estimated in a manner similar to the SPRHS. These results can be shared with stakeholders from local businesses and employees to elected officials. For suggestions of economists who might be able to assist with this type of evaluation effort, please contact the authors.

Publication 3692 (POD-12-21)

By Thomas Brewer, MSU Extension Service – Jefferson Davis County; William A. Sims, Department of Agricultural Economics; Thaddeus A. Webb, Department of Agricultural Economics; Kalyn T. Coatney, Department of Agricultural Economics; Rebecca C. Smith, Department of Agricultural Economics; James N. Barnes, Department of Agricultural Economics; Joy Fox Anderson, MSU Extension Service – DeSoto County; Gregory W. Biggs, MSU Extension Service – Madison County; and Alan Barefield, Department of Agricultural Economics.

The Mississippi State University Extension Service is working to ensure all web content is accessible to all users. If you need assistance accessing any of our content, please email the webteam or call 662-325-2262.